BenQ MA320U Review – The Best 32” 4K UHD Monitor for MacBook Users?

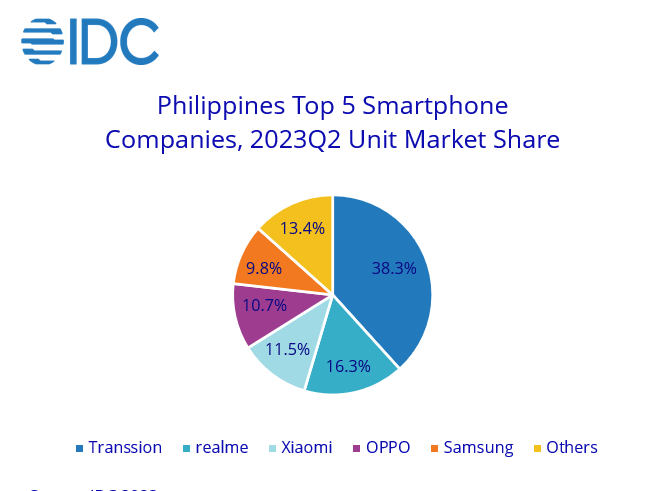

The Philippines smartphone market experienced a seismic shift during the second quarter of 2023, revealing an altered landscape of the Top 5 smartphone brands based off market share.

![]()

Transsion, realme, Xiaomi, OPPO, and Samsung have emerged as the front-runners in the market, with Transsion establishing a clear lead, according to the latest report by the International Data Corporation (IDC) Quarterly Mobile Phone Tracker.

Transsion’s extraordinary achievement in capturing an impressive 38% of total shipments has propelled them to the forefront of the smartphone race in the Philippines. This marks a transformative change in market dynamics, firmly establishing it as the leader among the Top 5 smartphone brands.

Securing the second position, realme demonstrated its mettle with innovative strategies and offerings that resonated well with consumers.

Meanwhile, Xiaomi, OPPO, and Samsung maintained their presence within the Top 5, attesting to their continued popularity and strategic relevance.

The overall market conditions witnessed a slight annual decline of 2.1% YoY, yet optimism prevailed with a promising quarter-over-quarter growth of 20.0%. This shift in momentum, following a series of quarters with double-digit reeductions, indicated a breath of fresh air within the industry.

“Despite a slowdown in inflation and an improving economic landscape in the Philippines, consumers remained cautious about spending due to higher commodity prices and economic uncertainties. As a result, we’ve observed eight consecutive quarters of annual contraction” explained Angela Medez, Senior Market Analyst for Client Devices at IDC Philippines.

Transsion emerged as the dominant player, capturing a substantial 38% share of total shipments in Q2 of 2023 and maintaining its leadership position for two consecutive quarters.

Within the Transsion umbrella, the sub-brand Tecno showcased impressive growth of 145% QoQ and 237% YoY. This surge was propelled by an expanded channel presence nationwide and a series of new model launches, particularly the Spark 10 series. These efforts drove remarkable growth of more than threefold in the ultra-low-end segment (below US$100), both on a quarterly and yearly basis.

“As the market anticipates sustained subdued conditions throughout the remainder of the year, IDC foresees heightened competition and expansion within the lower-price segments, as vendors work towards enhancing sales” added Medez.

YugaTech.com is the largest and longest-running technology site in the Philippines. Originally established in October 2002, the site was transformed into a full-fledged technology platform in 2005.

How to transfer, withdraw money from PayPal to GCash

Prices of Starlink satellite in the Philippines

Install Google GBox to Huawei smartphones

Pag-IBIG MP2 online application

How to check PhilHealth contributions online

How to find your SIM card serial number

Globe, PLDT, Converge, Sky: Unli fiber internet plans compared

10 biggest games in the Google Play Store

LTO periodic medical exam for 10-year licenses

Netflix codes to unlock hidden TV shows, movies

Apple, Asus, Cherry Mobile, Huawei, LG, Nokia, Oppo, Samsung, Sony, Vivo, Xiaomi, Lenovo, Infinix Mobile, Pocophone, Honor, iPhone, OnePlus, Tecno, Realme, HTC, Gionee, Kata, IQ00, Redmi, Razer, CloudFone, Motorola, Panasonic, TCL, Wiko

Best Android smartphones between PHP 20,000 - 25,000

Smartphones under PHP 10,000 in the Philippines

Smartphones under PHP 12K Philippines

Best smartphones for kids under PHP 7,000

Smartphones under PHP 15,000 in the Philippines

Best Android smartphones between PHP 15,000 - 20,000

Smartphones under PHP 20,000 in the Philippines

Most affordable 5G phones in the Philippines under PHP 20K

5G smartphones in the Philippines under PHP 16K

Smartphone pricelist Philippines 2024

Smartphone pricelist Philippines 2023

Smartphone pricelist Philippines 2022

Smartphone pricelist Philippines 2021

Smartphone pricelist Philippines 2020